In Mebane Faber’s paper, “Quantitative Approach to Tactical

Asset Allocation,” he builds a quantitative market-timing model that employs a

trend-following strategy with built-in risk management. Specifically, he

utilizes a moving-average-based trading system which is the most commonly used

trend-following method. The system rules are simple and are as follows:

Buy Rule: Buy when monthly closing price > 10-month Simple

Moving Average (SMA)

Sell Rule: Sell and move to cash when monthly closing price

is < 10-month SMA

At most, this system will rebalance monthly if a market is range-bound.

However, when using the 10-month SMA (near equivalent to the 200-day SMA) as a

trading signal, systems generally have a propensity for less turnover than

other actively managed strategies.

The converse, and one basis for comparison, of an actively

managed strategy is a passively managed system. Faber’s research compares the

model against a buy-and-hold (i.e. long) allocation to the S&P 500. When comparing

S&P 500 total returns to the Timing Model total returns during 1901-2012, the

model generates favorable risk-adjusted returns. The larger annualized returns

were a product of less volatility and smaller drawdowns than the buy-and-hold

method. Faber notes, “One of the reasons for the overall outperformance is the

lower volatility of the timing system. It is an established fact that high

volatility diminishes compounded returns.” Moreover, when comparing the S&P

500’s ten worst years from 1900-2012 to the timing model, the model offers

exceptional outperformance. This further exemplifies how

trend-following/market-timing models provide a reliable system for positive

long-term performance against a buy-and-hold strategy. Specifically, the timing

model avoids large, negative left-tail events in its return distribution, but

continues to capture positive outlier (i.e. right tail) events as well.

Next, Faber begins discussing how to implement the “Global

Tactical Asset Allocation” (GTAA) or timing model across five global asset

classes: US stocks, foreign stocks, bonds, real estate, and commodities. Funds

are allocated equally across each asset class (i.e. 20% each) and either

invested in the market or in cash (i.e. T-Bills). Since 1973, 80% of the time

GTAA has invested at least 60% of the portfolio, thereby offering an

opportunity to capture risk premium. Additionally, GTAA enhanced risk

management through lowering the maximum drawdown from -46% to -10% and an

investor would have experienced only one year with an annualized return of less

than -1.0%. Faber continues to note that while the sample from 1973-2005

performed well, out of sample testing of GTAA from 2006 through 2012 was

necessary to evaluate the efficacy of the strategy in practice. “Even though

[GTAA] only outperformed in three out of seven years, it beat the buy-and-hold

strategy by over 2% per year, with much less volatility and most importantly to

many investors, lower drawdowns.”

While GTAA offers attractive risk adjusted returns further

customization can be applied to the strategy to meet particular investor needs.

For example, the model can accommodate more (or less) asset classes, employ

alternative cash management strategies, and/or structure a portfolio with different

asset class weightings. For example, Faber provides another test of GTAA using

thirteen Exchange Traded Funds (ETF’s) to represent different asset classes as

well as market capitalization and style categories within equities. The results

improved performance by nearly 150 basis points (bps) per annum as well as

enhanced risk measurements. While using five ETF’s to represent the

aforementioned asset classes produced favorable results when compared against

an S&P 500 buy-and-hold strategy, Faber’s second test with thirteen ETF’s

provided even better results implying that there is ample room for improvement

and bespoke asset allocations to accommodate each investor.

Current Review of Five Asset Classes:

As SPX currently sits below its 10 month SMA, the Cambria

model would implore investors to have a full cash allocation in their

portfolios. Despite January’s swift selling the model gave a sell-signal with

the close of December 2015 being just below the 10-month SMA. Looking at the

chart below, past consolidations under this moving average have been

short-lived since the bull trend began in 2009. However, toward the end of 2007

the initial closes below the 10 month SMA were an early warning sign from price

action for what became a period of financial crisis in 2008. Currently, SPX is

exhibiting some indecision on a monthly basis with respect to its 10-month SMA.

After the August 2015 sell-off the index generated a sell signal. In October,

SPX staged a reversal* and offered a buy signal. Now, SPX has begun another

move below its 10-month SMA. Time will tell when this trendless behavior will

end and price begins to move in a sustained manner, but until that time

investors should understand that using Faber’s GTAA model will continue to

produce favorable performance statistics given its robustness in testing and

application.

In June 2015 the FTSE All-World Ex-US Index, represented by

VEU, began to show signs of weakness with a close below its 10-month SMA.

Selling accelerated in August of 2015 along with the US markets and the price

has stayed below its 10-month SMA ever since. Looking at the ten-year monthly

chart of VEU it can also be noted how lackluster the post-financial crisis

recovery was for the rest of the world as the 2007 highs were never cleared. In

fact, since the 2014 highs VEU has been forming a downtrend channel confirmed

by GTAA.

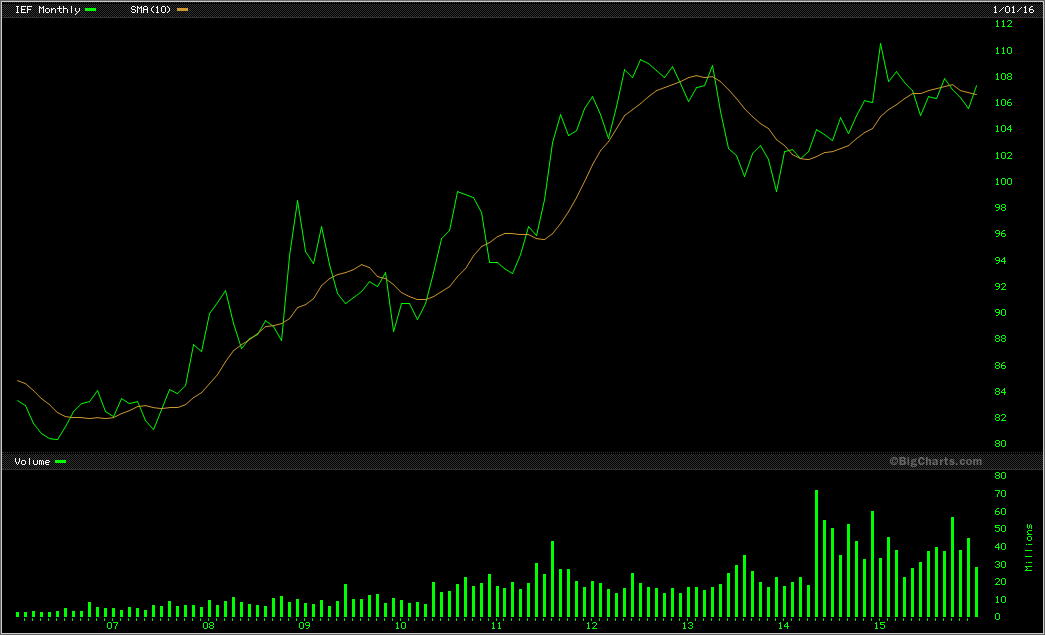

Presently, the 7-10 Year Treasury Bond market, IEF, is

providing a buy signal with January’s price action. Of course, this cannot be

confirmed until month-end. However, it would be a reversal of trend since a

sell signal was issued in October 2015. In the 10 year monthly chart there is a

clearly defined uptrend in place since the double-bottom in 2006-2007 and GTAA

has offered reliable entries and exits along the way.

Real Estate, as portrayed by VNQ, last issued a buy signal

in October 2015 but at this point in January is ready to close the previous position

with a fresh sell signal. Again, as with IEF, VNQ has been in a sustained

uptrend for several years with only a few entries and exits incurred by a GTAA

investor.

Commodities (DBC) have been in a prolonged downtrend since

the monthly close below the 10-month SMA in late summer 2014. The persistence

of the move has been impressive by many measures, but from this model’s

perspective the price has yet to close above the 10-month SMA. While the

decline in Crude Oil prices receives a majority of trader’s attention and is a

large component of DBC, the downtrend in commodities has been indifferent to

energy, agricultural, and metals commodities. This chart is arguably the best

example of how implementing GTAA adds value to an investor’s portfolio.

* See post entitled “MACD Confirmation and Divergence in

2015” for a look at the technical underpinnings developing in the market at

that time.

Note: All charts are

arithmetic in scale. Charts are line charts constructed using monthly closing

values.

JD

Comments

Post a Comment